The US Dollar disappointed this past week, with the US Dollar Index falling about 1.3% over the past 5 trading sessions. This was the worst performance since the end of January 2022. Could this be the start of a wider reversal for the US Dollar? That seems unlikely at this time, but there are a couple of reasons why the currency weakened.

All eyes are on the FOMC meeting minutes, where the document will reveal further details about this month’s 50-bases point rate hike. A hawkish tone coupled with confidence in the economy could bolster tightening bets. On Friday, the central bank’s preferred inflation gauge, the PCE core deflator, will cross the wires.

The coming week in the markets is likely to be more volatile as there are several data releases of high importance scheduled:

- On Monday, Germany’s Ifo business climate index will draw interest ahead of private sector PMI numbers on Tuesday.

- Tuesday the EU and US prelim private sector PMIs for May will be in focus. With the markets looking to second guess the Bank of England’s interest rate trajectory, expect the Services PMI to have the greater influence. On Tuesday, New Zealand’s retail sales will be in focus ahead of the RBNZ monetary policy decision on Wednesday.

- Wednesday starts with the New Zealand’s Official Cash Rate. Later in the day, the US monthly Core Durable Goods Orders will be announced. At night, the highly expected US FOMC Meeting Minutes will be announced.

- On Thursday, Canadian retail sales and the US quarterly preliminary GDP will provide the Loonie with direction. Later the US monthly Pending Home Sales are scheduled.

- Friday the US will release its monthly Core PCE Price Index and the Revised UoM Consumer Sentiment.

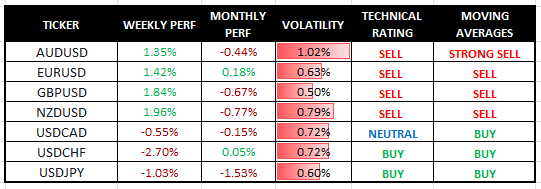

EUR/USD

The Euro bounced back to the important 1.05 level. We remain bearish as the pair will test parity.

FORECAST: SELL

Resistance: 1.0550, 1.0600, 1.0650

Support: 1.0500, 1.0450, 1.0400